The All-In-One Personalisation Engine for Financial Services

Make all digital banking interactions personalised and compelling from acquisition, to activation, to engagement.

LET'S GET STARTED

Make all digital banking interactions personalised and compelling from acquisition, to activation, to engagement.

LET'S GET STARTED81%

Satisfied Users

7x

Sales Conversions

-22%

Reduced Customer Support

OUR CLIENTS

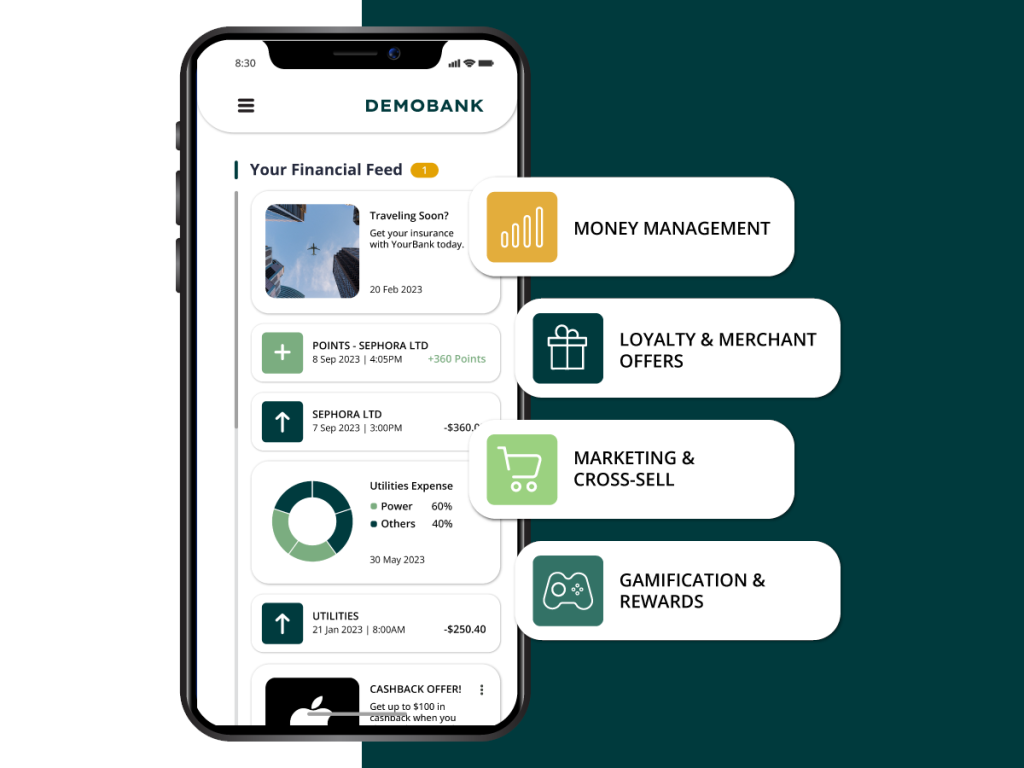

Powered by real-time data analytics and behavioural science, the Moneythor Solution delivers un-matched, data-driven and personalised experiences to customers across all digital banking channels. Examples of these include money management nudges, budgets, savings goals, predictive forecasts, financial literacy material, referral campaigns, gamified experiences, loyalty programs and more.

EXPLOREAcquisition is good. Activation is better. Engagement is best.

Rapidly grow your customer base by implementing a range of Moneythor use cases such as unified multi-product referrals and social incentives to drive increased acquisition.

METRICS WE DRIVE:

• Increased acquisition

• Reduced CAC

Build a profitable and active user base by delivering tailored and gamified journeys and campaigns right upon customer’s onboarding.

METRICS WE DRIVE:

• Increased account activation and deposits

• Increased card activation and usage

Nurture long lasting engagement with customers through the integrated implementation of personalised use cases including personal financial management (PFM), financial wellbeing programs, sustainability insights and cross-product loyalty campaigns.

METRICS WE DRIVE:

• Engagement

• Referrals

• Retention

Make customer’s financial lives easier and drive real engagement with modern Personal Financial Management (PFM) features.

Provide captivating interactions to clients, aid them in improving their financial well-being while simultaneously boosting retention and loyalty. PFM use cases natively offered by the Moneythor solution include advanced transaction categorisation and enrichment techniques, spending budgets, savings goals, predictive cashflow analysis, as well as the production of tailored contextual insights.

Learn moreCustomer needs and expectations change. Manage this with a fully flexible and agile engagement engine.

Don’t waste time, get to market quickly and efficiently.

No more siloed experiences across multiple platforms. One powerful engagement engine can do it all.

When we say real-time, we mean really real-time.

Next-level personalisation tailored to the individual.

Moneythor was founded 10 years ago. We know what works and what doesn’t.

Profitable business that works with a strategic mindset. We get things done without distraction.

“We are dedicated to providing New Zealanders with truly customer-centric imoney management solutions to help them achieve their financial goals. We were pleased to find in Moneythor a technology solution provider sharing our vision around financial wellbeing, and to implement their configurable platform to power several of Savvy’s best-in-class and highly engaging experience for our customers.”

Diana Papadopoulos, Chief Customer Officer, Booster

“Our partnership with Moneythor gives Ta3meed a competitive edge in enriching its PO Financing offer with smart loyalty features and personalised recommendations, differentiated through innovation, customer experience and reliability.”

Mohamed Alomayyer, CEO and Co-Founder, Ta3meed

“Our personal recommendation service “LiFit” has been implemented with the Moneythor solution. With LiFit, we are going to achieve better communications across both physical and digital channels, rebuild closer relationships with our customers, and provide improved customer experiences.”

Jiro Yasuda, Corporate Officer & General Manager, IT Management Division, The Ogaki Kyoritsu Bank

Moneythor, the leading provider of real-time, personalised engagement and loyalty solutions for banks and fintech [...]

READ MORE

Moneythor announces strategic partnership with YOUGotaGift to incorporate their extensive digital gift cards catalogue to [...]

READ MORE

Join Moneythor CEO, Olivier Berthier, for an insightful exploration of the transformative influence of AI/ML [...]

READ MORE

What are Prize-Linked Savings Accounts (PLSAs)? Prize-linked savings accounts (PLSAs) merge the conventional concept of [...]

READ MORE

In 2013, we started with a mission to improve the customer digital banking experience with [...]

READ MORE

Since partnering in 2018, Moneythor and ANZ have worked together on numerous use cases and [...]

READ MORE

The current state of play In the midst of a cost-of-living crisis and with rising [...]

READ MORE

Open Banking involves the secure sharing of financial data and services with third parties through [...]

READ MORE

According to the Consumer Financial Protection Bureau, financial wellbeing is defined as “a state of being [...]

READ MORE

Personalisation has and continues to be a key area of focus for the banking sector [...]

READ MORE

As we approach 2024, digital banking is set for substantial changes, influenced by emerging trends [...]

READ MORE

Singapore, 15 November 2023 – Moneythor, the leading provider of personalisation and digital engagement solutions [...]

READ MORE

Booster goes live with Moneythor to deliver innovative and personalised features for its new Savvy [...]

READ MORE

The current state of play In today’s competitive banking landscape, there is an imperative for [...]

READ MORE

The value of incentivised referrals With many financial institutions vying for market share, the pressure [...]

READ MORE

The Moneythor team is excited to be exhibiting at this year’s Singapore FinTech Festival (SFF), [...]

READ MORE

"*" indicates required fields

"*" indicates required fields